1. For Sale By Owner (FSBO)

For Sale By Owner (FSBO) properties are homes that the seller lists and sells independently, without the help of a real estate agent. While many FSBO transactions are legitimate, some can be used by scammers to avoid professional oversight and regulation. Without a real estate agent or attorney involved, the buyer may not have access to the proper legal protections or guidance during the transaction.

Zillow recommends that buyers consider hiring a real estate attorney when purchasing an FSBO property to ensure that all documents are accurate and legally binding. A lawyer can review contracts, ensure that the seller has clear title to the property, and help with the closing process. Although buying FSBO can sometimes result in a good deal, it is essential to approach it with caution and due diligence. The absence of a professional agent could lead to missed red flags that might otherwise be caught. To learn more about FSBO transactions, visit Zillow.

2. Earnest Money Deposit

An earnest money deposit is a good faith deposit made by the buyer to demonstrate their serious intent to purchase a property. This deposit assures the seller that the buyer is committed to the deal. Unfortunately, some scammers may misrepresent this deposit as a non-refundable fee that they can pocket, so it is vital to understand how and where your deposit is being held.

Typically, the earnest money is placed in an escrow account, which is managed by a neutral third party. This helps ensure that neither the buyer nor the seller can access the funds without meeting certain conditions. As such, it’s crucial to work with trusted professionals to avoid potential scams. Investopedia emphasizes that the deposit should always go into a legitimate escrow account to ensure proper handling. Therefore, buyers must confirm that the escrow account is well-regulated and that it holds the deposit until the deal is finalized. You can read more on how earnest money works on Investopedia.

3. Escrow Account

An escrow account serves as a neutral holding space for funds during a real estate transaction, ensuring that both the buyer and seller meet their obligations before the transfer of property takes place. This account provides protection to both parties by safeguarding the funds until all terms of the agreement are satisfied. Unfortunately, scammers sometimes create fake escrow accounts to steal money from unsuspecting buyers. To avoid this, it is essential to verify the legitimacy of the escrow account by consulting with your bank or a trusted real estate agent.

You should never release funds into an account without confirmation that it is authentic and secure. The Consumer Financial Protection Bureau (CFPB) provides helpful guidelines on how to identify secure escrow services, offering valuable advice on safeguarding your finances. Always ask for documentation that proves the legitimacy of the escrow account. A trustworthy agent or attorney can help ensure that the account is properly established. To learn more about escrow accounts and their importance, visit the Consumer Financial Protection Bureau.

4. Contingency Clause

Contingency clauses are conditions written into a sales contract that must be met for the transaction to proceed. These contingencies can cover a variety of factors, such as property inspections or securing financing. However, some unscrupulous sellers or agents might pressure buyers to waive these protections in order to expedite the sale. It’s important not to give in to such pressure without fully understanding the potential risks involved. For example, waiving the inspection contingency could mean purchasing a property with hidden structural issues or safety concerns.

According to Nolo, it’s always wise to consult a real estate attorney before agreeing to remove any contingency clauses from the contract. These legal professionals can guide you on whether waiving a contingency is in your best interest. A well-drafted contract that includes solid contingencies can provide essential protection. Before finalizing any agreements, ensure that you understand the implications of each clause in your contract.

5. Dual Agency

Dual agency occurs when one real estate agent represents both the buyer and the seller in a transaction. While this arrangement may seem convenient, it can create conflicts of interest, as the agent has the responsibility to both parties. This situation can lead to biased advice or unfair treatment, favoring one party over the other. Scammers may exploit dual agency to pressure buyers into agreeing to unfavorable terms without proper representation. Working with a dedicated agent who solely represents the buyer’s interests can help avoid such conflicts.

Realtor.com advises that buyers work with an exclusive buyer’s agent to ensure they are fully supported throughout the process. This type of representation ensures that the agent’s duty of loyalty is to the buyer alone, reducing the risk of potential manipulation. Exclusive buyer’s agents can offer expert advice, negotiate on the buyer’s behalf, and help avoid situations where the seller’s interests take precedence. For more information on dual agency, check out Realtor.com.

6. Deed Fraud

Deed fraud is a form of property theft where scammers forge or transfer property ownership without the rightful owner’s consent. This can be done by altering public records or filing fraudulent documents to change the title of the property. Deed fraud is particularly dangerous because it may go unnoticed for some time, leaving the rightful owner unaware that their property has been stolen. To protect yourself from such fraud, it’s important to check your local property records regularly to ensure no unauthorized changes have been made.

The Federal Trade Commission (FTC) recommends monitoring public records as a preventive measure against deed fraud. Many states now offer fraud alert services that notify property owners when changes are made to their title. If you suspect any fraudulent activity, contact local authorities immediately. Taking proactive steps to protect your property rights is key to avoiding becoming a victim of deed fraud. You can learn more about deed fraud prevention from the Federal Trade Commission.

7. Title Insurance

Title insurance is a type of insurance policy that protects the buyer from any disputes or claims regarding the ownership of the property. It ensures that the property title is free from liens, encumbrances, or other legal challenges that could affect ownership. However, some scammers may sell fake title insurance policies, leaving buyers vulnerable to future legal complications. To prevent falling for these scams, it is essential to verify the legitimacy of the title insurance provider. Always check the insurer’s credentials and consult with your state’s insurance department for validation.

ALTA (American Land Title Association) offers a comprehensive guide to help buyers choose a reputable title insurance company. They emphasize that title insurance should be obtained from a licensed and trustworthy insurer to protect your interests. If you are unsure about the legitimacy of an insurance policy, seek advice from a legal professional or trusted agent. For more details on title insurance, visit ALTA.

8. Predatory Lending

Predatory lending refers to unfair loan practices designed to exploit borrowers, often through high-interest rates, excessive fees, or misleading terms. This type of lending is particularly harmful to buyers who may not fully understand the loan terms or are desperate to secure financing. Scammers may use aggressive tactics to push buyers into accepting these detrimental loans. The Department of Housing and Urban Development (HUD) warns consumers to carefully review all loan documents before signing. HUD also recommends that buyers shop around for better loan options and seek the advice of a financial advisor.

Predatory lenders often target vulnerable individuals, so being informed and cautious is essential in avoiding these deceptive practices. If something seems too good to be true, it probably is. Always be wary of loan terms that seem unusually favorable but include hidden fees or unreasonable conditions. To learn more about avoiding predatory lending, visit the Department of Housing and Urban Development.

9. Adjustable-Rate Mortgage (ARM)

An Adjustable-Rate Mortgage (ARM) is a type of home loan where the interest rate starts lower than that of a fixed-rate mortgage but can increase significantly over time. Scammers may misrepresent ARMs as fixed-rate loans, luring buyers with an initially low interest rate that later spikes, making monthly payments unaffordable. It is crucial to understand the full terms of an ARM before committing to this type of loan. Always ask the lender about potential rate adjustments and how often the interest rate may change.

Bankrate suggests that borrowers carefully review the loan terms and consider whether an ARM is the right choice based on their financial situation. Consulting with a trusted financial advisor can help clarify whether an ARM is a smart option, particularly if you plan to stay in the home for many years. The risk of rate increases can be difficult to predict, so understanding the details of the loan is essential. To get more insights on ARMs, visit Bankrate.

10. Flipping Fraud

Flipping fraud occurs when a property is bought and sold at inflated prices, often through fraudulent appraisals or misleading renovations that hide serious issues. Scammers may conduct fake repairs or exaggerate the value of the property to deceive the buyer into paying far more than the home is worth. To protect yourself from falling victim to flipping fraud, always verify the property’s appraisal and have the home inspected by a certified professional before buying.

The Appraisal Institute advises that buyers be diligent about ensuring the appraisal reflects the true market value of the property. If the appraisal seems unusually high or doesn’t match comparable homes in the area, it could be a red flag. Additionally, it’s wise to inspect the home thoroughly to ensure that repairs or improvements were made properly and not just to cover up defects. For more advice on property appraisals and how to avoid fraud, visit the Appraisal Institute.

11. Loan Origination Fee

A loan origination fee is charged by lenders to cover the cost of processing a loan application. This fee can vary depending on the lender and the loan amount, but it is typically a percentage of the loan value. Unfortunately, fraudsters may attempt to overcharge buyers or include unnecessary fees in an attempt to inflate their profits. To protect yourself from this type of fraud, it is essential to compare the loan origination fees with the standard rates in your area.

Consumer Reports recommends reviewing all fees listed on a loan agreement to ensure that they are reasonable and in line with industry norms. Additionally, be sure to question any fees that seem unusually high or unexplained. It is always a good idea to consult with a financial advisor to help assess whether these fees are legitimate. By being vigilant and well-informed, you can avoid falling victim to fraudulent lenders. Learn more about typical loan origination fees here.

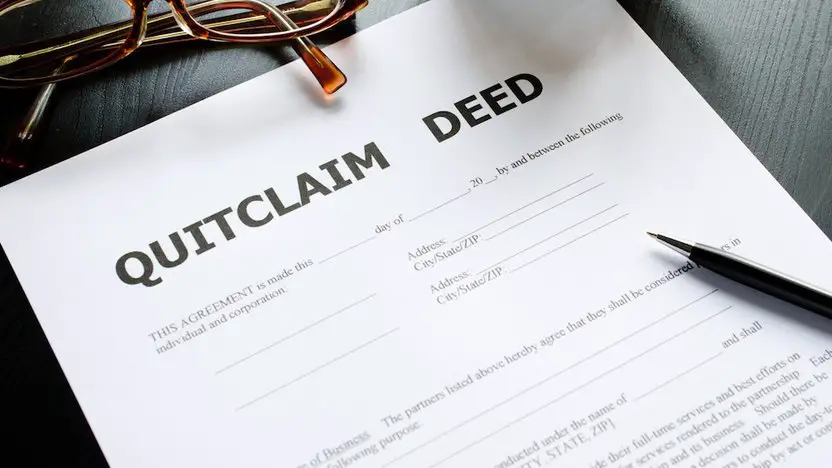

12. Quitclaim Deed

A quitclaim deed is a type of legal document used to transfer ownership of property, but it does not guarantee that the title is free from claims, liens, or other encumbrances. This type of deed can be risky for buyers since it offers no assurances regarding the property’s legal status or potential financial liabilities. Scammers may use a quitclaim deed to offload properties with hidden legal issues, such as unresolved debts or disputed ownership.

For this reason, it is crucial to carefully review any deed before accepting ownership of the property. LegalZoom recommends using a warranty deed instead, as it offers greater protection by guaranteeing that the title is clear of any encumbrances. Always work with a qualified attorney or title company to ensure that the deed transfer is legitimate and the property title is free from hidden complications. Find out more about quitclaim deeds and alternatives here.

13. Mortgage Pre-Approval

A mortgage pre-approval letter is a document from a lender that confirms a buyer’s financial readiness to purchase a home. This letter is often used to demonstrate to sellers that the buyer is serious and capable of securing a loan. Unfortunately, scammers may create fake pre-approval letters in an attempt to gain access to sensitive financial information or to deceive sellers into thinking they have a qualified buyer.

It is essential to verify the authenticity of any pre-approval letter before taking further steps in a real estate transaction. Experian recommends contacting the lender directly to confirm the legitimacy of the pre-approval and ensure that the buyer has undergone the proper financial review. Never rely solely on a document without cross-checking with a reputable source. Additionally, be cautious of lenders that pressure you into rushing the pre-approval process. Learn how to verify pre-approvals here.

14. Closing Costs

Closing costs refer to the various fees that are due at the completion of a real estate transaction. These costs can include taxes, lender fees, title insurance, inspection fees, and other related expenses. However, scammers may inflate these costs or charge for services that were never provided, such as nonexistent inspections or unnecessary paperwork. To avoid being overcharged, it is crucial to request a detailed, itemized breakdown of all closing costs before finalizing the deal.

Rocket Mortgage advises that buyers should carefully review each item on the list and ensure that it aligns with the services provided. If something seems out of place or unusually high, do not hesitate to ask for clarification or seek a second opinion. By staying informed and asking questions, buyers can avoid paying inflated closing costs. Get tips on avoiding closing cost scams here.